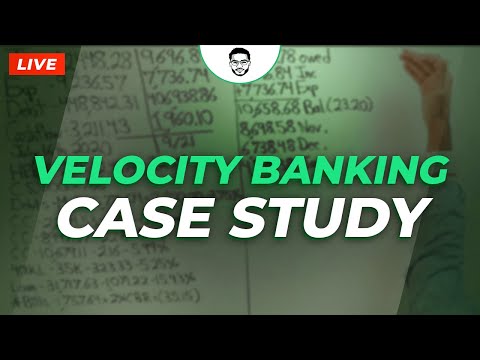

True" Music, hello and welcome! Velocity banking students, kingdom citizens, loyal subscribers, and all the new people, how are you doing? My name is Denzel Rodriguez, your personal finance key to the 21st century. Today, I have a velocity banking scenario for you regarding a mom. - We're going to be serving a mom today on the board here. We're going to be doing velocity banking to pay off debt extremely fast, leveraging a personal line of credit to our advantage. This way, we can offset our interest cost of borrowing, increase cash flow, build credit score, lower expenses, and retain cash flow. Build my beautiful kingdom, amen, in the name of Jesus. - I am super excited to share this scenario with you, and we're also going to compare our results to the debt snowball concept. What I'm going to do is do velocity banking conservatively. I'm going to use conservative numbers, okay? And then I'm going to put it up against the debt snowball concept, and I'm going to be aggressive with the debt snowball con. So, I'm going to give that snowball some leverage over velocity banking, and let's see how the results pan out. Let's really put this to the test. - So, let's dive into the details. For major numbers, individual mom making $4,250 a month. Expenses currently $3,682. Total debt is $70,491.89. My starting cash flow is $568 per month. I have a personal, unsecured revolving line of credit calculated simple interest for $20,000 at a 7.49% interest rate. - We are in the state of New York, specifically in Brooklyn. We have a credit union called Santander Bank that covers that area, and there's another bank in the up Northland, maybe the Long Island area, called Bethpage Federal Credit Union. These are nice-sized credit unions that serve...

Award-winning PDF software

Video instructions and help with filling out and completing Dd 1750